The escalating military conflict in the Middle East has created serious security risks across some of the world’s most important shipping corridors, both directly and indirectly impacting major trade lanes, capacity pressure and oil prices.

The “dual blockade” reality: Both the Strait of Hormuz and Red Sea routes are effectively compromised, forcing a massive, structural shift to Cape of Good Hope routing for Asia-Europe trade.

Capacity and rate volatility: The detour around Africa adds 10–15 days to voyages, absorbing roughly 2.5 million TEU of global capacity and driving surcharges and rate hikes.

Energy-driven inflation: With Brent Crude stabilized above $110 and diesel prices up 30%, logistics providers are facing extreme margin pressure.

Air freight crisis: The suspension of major Gulf hubs (Dubai, Doha) has eliminated critical belly capacity, causing air freight rates to surge and removing the traditional “safety valve” for delayed ocean cargo.

Strategic resiliency: Shippers must move from “just-in-time” to “just-in-case” strategy, by building inventory buffers, stress-testing lead times against a 6-week disruption model, and securing capacity 4–6 weeks in advance.

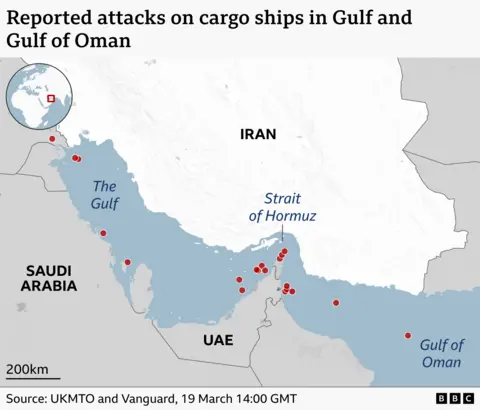

What’s happening in the Strait of Hormuz?

The current escalation centres on the Strait of Hormuz, a narrow passage between Iran and the Arabian Peninsula that serves as one of the world’s most strategically significant trade corridors. Around 20% of global oil consumption passes through it every day, along with containerised cargo serving Gulf ports.

Since the start of March, 100 ships have passed through the Strait of Hormuz; prior to the war, around 138 ships passed through the strait each down – meaning daily traffic is down approximately 95%.

The initial “wait and see” approach from global carriers has rapidly shifted into a coordinated, large-scale exit from the Persian Gulf. For operators who were just beginning to reintroduce Suez Canal transits after years of Red Sea instability, this conflict represents a dual blockade that has effectively closed the most direct water bridge between East and West.

Immediate operational withdrawals: The response from major alliances has been swift and severe. MSC, Maersk, and Hapag-Lloyd have all issued End-of-Voyage (EoV) declarations for cargo currently in transit to the Arabian Gulf. Under these declarations, vessels are discharging containers at the nearest safe ports rather than proceeding into the high-risk zone. Booking stops and cargo suspensions now apply to nearly all major lines serving the Upper Gulf, as insurers withdraw war-risk coverage for the region. As a result, Asia–Europe services have systematically reverted to the Cape of Good Hope routing.

The capacity and reliability crunch: The decision to bypass the Middle East and Suez Canal entirely is not a simple detour; it is a structural drain on global shipping resources:

In just the first week of the crisis, disruption affected approximately 130 container vessels, representing roughly 470,000 TEU – or 1.9% of the global fleet.

Rerouting around Africa adds roughly 10–15 days to a standard head-haul voyage. As these rotations lengthen, the “effective capacity” of the global network contracts, creating equipment shortages in Asia even for routes not directly passing through the conflict zone.

According to recent Xeneta data, the average delay on Middle East trade has spiked to +6.72 days, while on-time reliability has collapsed to a staggering 10%.

Transhipment under pressure: With the Gulf’s primary hub, Jebel Ali, seeing a 40% drop in vessel calls due to its proximity to the conflict, cargo is being “pushed out” to regional alternatives. Salalah, Colombo, and Jeddah are now facing immense transhipment pressure. DP World has moved to mitigate this by opening emergency land service corridors to link Jebel Ali with Saudi hubs like Dammam. However, the operational complexity of moving Jebel Ali’s 15.5 million annual TEU via land and secondary ports remains one of the greatest logistical hurdles of the 2026 crisis.

This is no longer a localised Middle East issue. The diversion via the Cape of Good Hope is absorbing the world’s spare vessel capacity, meaning even shippers on Trans-Pacific or Intra-Asia lanes should prepare for “contagion” effects in the form of rising rates and equipment imbalances.

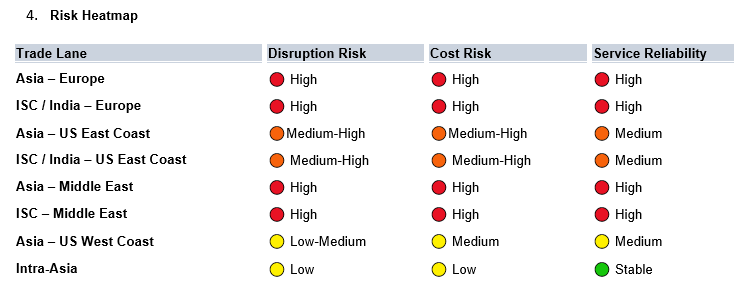

How does disruption compare across trade lanes?

Disruption varies significantly by route, depending on proximity to the Gulf and reliance on Suez Canal transit.

Source: ECU Worldwide – 04.03.26

Asia–Europe and India–Europe lanes are the most exposed. These services depend on the Suez Canal corridor or operate close to the affected region. Disruption risk, cost risk and service reliability concerns are all elevated on these routes.

Middle East–bound cargo faces the most direct disruption, as carrier operations and routing decisions are being actively reassessed.

Asia–US routes are less directly exposed but are not immune. As vessel rotations lengthen and global capacity tightens, indirect pressure builds. Asia–US East Coast services, which may transit Suez, carry medium-high risk. Asia–US West Coast routes face lower disruption but could still see cost and reliability effects.

Pacific and intra-Asia routes remain relatively stable, reflecting their distance from the conflict zone.

How does the conflict impact air freight?

Middle Eastern aviation hubs are currently operating under huge operational strain. While airports like Dubai (DXB), Doha (DOH), and Abu Dhabi (AUH) have avoided total permanent closure, they are operating via strictly controlled air corridors that have slashed commercial capacity.

The statistics for March 2026 highlight a historic supply-side shock:

Air cargo capacity from the Middle East and South Asia (MESA) origin region has plunged by 48% year-on-year as of mid-March.

Because roughly 25% of China–Europe air freight typically transits through Gulf hubs, this lane has seen a 26% to 39% drop in available cargo tonne-kilometres (ACTK).

With over 27,000 flight cancellations recorded across Emirates, Etihad, and Qatar Airways since the conflict began, the “belly hold” space that retailers rely on for smaller, urgent shipments has effectively vanished.

It isn’t just a lack of planes; it’s a lack of efficiency. To avoid restricted airspace over Iran and Iraq, freighters are being rerouted through Central Asian or Southern Indian corridors, adding 2–4 hours of flight time. This requires more fuel, which in turn creates payload penalties—aircraft must carry less cargo to stay under maximum takeoff weight.

Oil and energy price disruption

One of the widest and most difficult-to-avoid issues is the sharp and sustained spike in energy prices, now feeding through into logistics costs at every level. The current crisis has been described by the International Energy Agency (IEA) as the largest supply disruption in the history of the global oil market, surpassing the shocks of the 1970s.

Crude oil and diesel

Brent crude has surged by roughly 50–60% since the conflict began on 28 February. While it briefly touched a high of $119 a barrel earlier this month, prices as of March 23, 2026, are trading above $113 per barrel following new threats to regional energy infrastructure.

To combat this, the IEA recently coordinated the largest-ever release of emergency oil stocks, committing 400 million barrels to the global market. Despite this, fuel prices remain at multi-year highs:

British wholesale gas prices surged to 171p per therm following the escalation—the highest level since 2022.

Economists warn that if these prices persist into the summer, UK inflation could head toward 5%, forcing the Bank of England to consider interest rate hikes rather than the previously expected cuts.

As diesel remains the single largest operating cost for UK hauliers, these “second-round” inflationary effects will inevitably be passed from the supply chain down to the end consumer.

How the impact evolves over time

The logistics impact of this war will depend largely on how long it goes on. A short-lived escalation creates volatility but is manageable. A prolonged crisis reshapes the entire operating environment:

In the first two weeks, the impact is localised: precautionary routing changes, insurance reviews and short-term schedule volatility.

By four to six weeks, the network effects start to build. Longer voyages disrupt vessel rotations and hub connectivity. Capacity tightens noticeably, schedule reliability weakens and freight rates begin to move upward.

At the six-month mark, the industry enters structural adjustment. Carriers redesign service networks, shipping alliances rebalance capacity and alternative routings become the default rather than the exception.

If disruption persists for a year or more, it will likely lead to strategic supply chain shifts, with companies redesigning sourcing strategies, building inventory buffers and fundamentally rethinking their transport networks.

What shippers can do now

The situation is fluid, but being proactive can help reduce your level of disruption. In working with our retail clients, we’ve focused on concrete steps to reduce their exposure.

Stress-test your lead times. Model your delivery timelines against extended routing scenarios, including Cape of Good Hope diversions, transhipment via alternative hubs, and longer air corridors. If your planning assumptions are built around Suez Canal transit times, they may already be out of date.

Review your priority inventory. Identify which SKUs are most exposed to Gulf-related disruption and consider building buffer stock where possible. The cost of holding additional inventory is typically far lower than the cost of stockouts during a prolonged disruption.

Secure capacity early and prepare for surcharges. In a tightening market, early movers have more options. If you anticipate needing ocean or air freight capacity on affected lanes in the coming weeks, work with your freight forwarder to book now rather than waiting for the situation to clarify.

Consider your routing flexibility. Consider whether your supply chain accommodates alternative modes, such as rail, sea-air combinations, or different transhipment ports.