Beyond the blockade: Why modal flexibility is redefining global trade

Scroll to find out more

Scroll to find out more

The blockade of the Strait of Hormuz has exposed the critical vulnerability of global supply chains that rely on a single maritime corridor. In doing so, it has accelerated a structural shift toward modal flexibility that was already underway.

Over eight weeks into the Strait of Hormuz blockade, the crisis continues to be volatile and unpredictable for shippers. Crude is fluctuating, reaching highs of more than $100 a barrel. The Pentagon, according to Associated Press sources, estimates six months of mine-clearing before normal usage can resume, even after a ceasefire. It seems a resolution in the near future is unlikely.

For a strait that handles a relatively narrow slice of containerised China-Europe trade, the secondary effects have been remarkable. Bunker prices have hit all time highs, while war-risk insurance has climbed from 2% to roughly 3% of vessel value. Hapag-Lloyd’s chief executive, Rolf Habben Jansen, told investors recently that the closure was costing the carrier around $50 million per week in additional fuel alone.

Building a cost-focused global supply chain around a few ocean trade lanes creates extreme exposure to disruption, cost-variability and uncertainty. So, eyes across the supply chain world are looking to alternatives.

For decades, container shipping’s economics shaped the geography of global trade. Ocean freight was cost-effective, scaled beautifully, and made most overland alternatives uncompetitive on anything except urgency – a role filled mostly by air freight.

Today, over two months into the Middle East conflict, carriers are forced into layering emergency fuel surcharges on top of base rates as they face wild swings in prices. Habben Jansen has been candid about the rationale, quoted in The Loadstar: “We do that in order to recover our costs, not to make money. Anyone who calculates those fuel surcharges will recognise that, in the end, those amounts are actually pretty reasonable.” And while few in the industry would argue this point, as US freight forwarder Crane Worldwide noted in market analysis recently, the cumulative effect is that surcharges reduce the predictability of total landed costs.

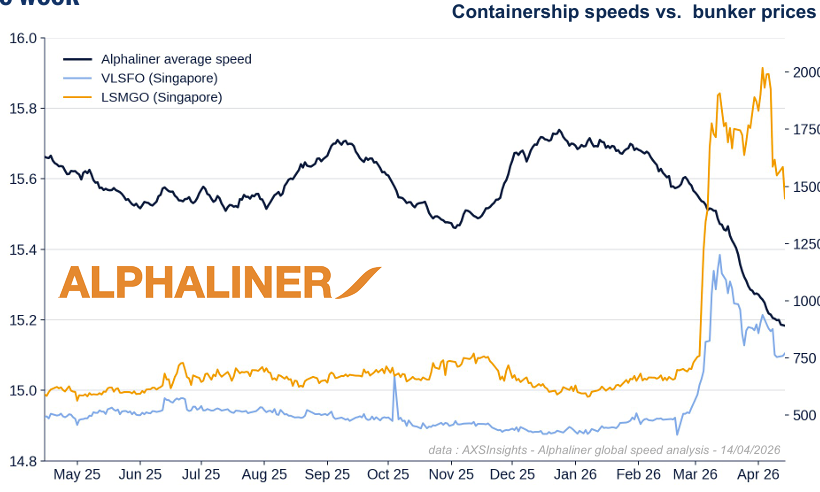

There is also the question of time. Alphaliner data shows the average containership speed fell to 15.18 knots on 14 April 2026, the lowest reading since March 2023, and a 2.3% decline on Q4 2025. This is likely due to slow-steaming to reduce fuel use, concentrated entirely after 28 February. Combined with a 14 day detour around the Cape of Good Hope, and 5-7 days of berth congestion at hubs like Singapore and Tangier Med, total Asia-Europe lead-time extensions now frequently exceed 21 days.

The industry is seeing some interesting responses to this landscape. For example, carriers facing the disruption due to the conflict in the Middle East have been offloading cargo at safer hubs, such as Salalah in Oman, Khorfakkan and Jeddah, and trucking the final leg overland into the Gulf.

What started as a workaround is showing signs of permanence; in late March, Saudi Arabia Railways launched a new 1,700-kilometre rail freight corridor connecting King Abdulaziz Port at Dammam, Al-Jubail Commercial Port and King Fahd Industrial Port up to the Al-Haditha border crossing with Jordan. Each train carries more than 400 containers. SAR moved 30 million tonnes of freight in 2025, up from 24 million in 2023, removing two million truck journeys from Saudi highways in the process.

This also recontextualises the value of a longer gestating project: the $7 billion Saudi Landbridge, on which construction began in 2025: more than 1,400 kilometres of new and upgraded track linking Jeddah on the Red Sea to Dammam on the Gulf. Once operational, it will be the first direct rail link between the two seas, allowing ocean cargo bound for Gulf markets to land at Jeddah and reach Dammam without any vessel transiting the Strait of Hormuz at all.

Saudi Arabia has spent the better part of a decade trying to position itself as a logistics hub through Vision 2030. A blockade in the Strait next door is doing the work that subsidies could not, drawing attention to lesser used routes and providing a business case for shippers.

The clearest signal that investments into overland routes are a structural rather than temporary shift comes from the carriers themselves.

Gemini Cooperation has officially and permanently redeployed vessels via Europe into Jeddah to serve Middle East-Asia routes, replacing its old feeder services. The Cape of Good Hope detour, which adds roughly 21-28 days to a standard Asia-Europe loop, has created a vessel deficit of three to four ships per service that carriers are absorbing structurally through more capacity on the lane, not through shorter waits for the Suez Canal to reopen.

Drewry’s senior container analyst Simon Heaney has described the underlying shift: liner networks are moving from being cost-optimised to risk-managed and resilience-focused as a permanent feature. This reflects the demands of shippers: when uncertainty becomes constant, carriers sell peace of mind, wherever the route takes them.

As ocean contends with a more complex, risky environment, the next alternative for bulky cargo is rail – and the data suggests shippers are noticing.

China-Europe Railway Express moved 352,100 TEU in January and February 2026, up 25.2% year-on-year. The Eurasian Rail Alliance had reported that 2025 was actually a difficult year for rail, with volumes falling 18% as lower ocean rates clawed back share. The early 2026 numbers represent a meaningful reversal, and they were recorded before the regional conflict fully reshaped the picture.

The Trans-Caspian Middle Corridor is growing even faster. Container train traffic through Kazakhstan rose 34.4% in Q1 2026 versus the same period in 2025. Capacity along the corridor is targeted to reach 10 million tonnes by 2027 and 15 million by 2030, supported by a €22 billion EU Global Gateway commitment to Central Asian connectivity in 2024-2025 alone.

Rail’s old reputation as a black box of limited tracking, gauge-change delays, and opaque scheduling is also less and less deserved. Technology investments such as the integration of real-time GPS and environmental tracking devices in containers have closed much of the visibility gap with ocean.

For shippers with the right cargo profile, it has become a serious option for the first time in years.

The 2021 Suez blockage, the Red Sea crisis, the ongoing Hormuz disruption – shippers are functioning in a landscape defined by disruption. That means that resilience now looks like modal flexibility: the ability to compare ocean, rail, and air across cost, time, and risk in real-time, shifting allocations as conditions change.

Historically, switching modes was a manual nightmare of rebuilding cost models and chasing disparate schedules. AI has eliminated this friction. On the Zencargo platform, we see this active resilience in the data: users aren’t just logging in to check a status; they are deeply interrogating their supply chains. Over the past 24 months, we’ve seen a 20% increase in active users, with organisations now maintaining over 20 users monthly on average. This isn’t just one person tracking a box – it is entire teams collaborating within the platform to manage complexity.

Today our technology enables shippers to move beyond simple tracking. They are leveraging networked data to model the all-in cost of a booking against multi-modal alternatives in minutes. We enable a new kind of strategy: planning the best route for every shipment, rather than picking a path and sticking with it regardless of environmental factors. By tracking high-density SKU counts and complex shipment volumes in a single view, our AI-powered co-pilot, Luca, allows for the macro move to be executed with micro precision.

For UK retail brands, international expansion has moved from long-term ambition...

Zencargo platform newsletter. Explore our latest AI innovations and updates.

Discover how AI is transforming global supply chains from reactive operations i...