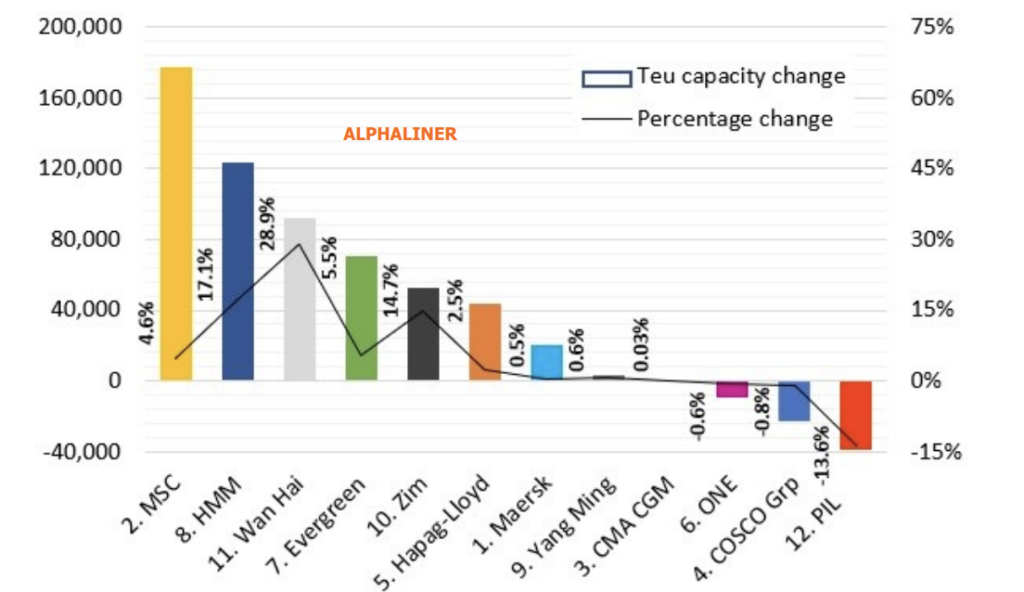

Who’s winning the race to add new capacity to the market?

Source: Alphaliner

A new report from Alphaliner highlights the rush from liner operators to add more capacity during this era of peak rates. A comparison of the top 12 carriers’ capacity between January 1 and today identifies five leaders in adding capacity.

MSC and Wan Hai have been the most successful buyers of tonnage on the second market

Zim has been active in the charter market finding extra tonnage for its new Transpacific services.

HMM and Evergreen happened to have a lot of new building deliveries planned for the first half of this year, luckily.

MSC has been the fastest growing operator this year in terms of actual slots (+177,691 teu) as the Geneva-based carrier took delivery of two more 23,656 teu ships. Meanwhile, Maersk’s capacity growth in H1 still remains limited to 0.5% of its current size, putting MSC on course to become the new number one in liner shipping.

Want freight market updates delivered straight to your inbox every week?

Ocean

Asia → North America

Rates

Hapag-Lloyd has announced a new PSS effective July 18 applicable for all dry, reefer, flat rack and open top containers from East Asia to US and Canada:

USD 1000 per all 20′ container types

USD 2000 per all 40′ container type

Capacity

Maersk will launch two new weekly services, the TPX and TP20, to add more capacity. These services will be independent of the 2M alliance.

TPX will call at Yantian and Ningbo in China, finishing at LA.

TP20 will call at Vung Tao, Vietnam, Ningbo and Shanghai in China and Norfolk and Baltimore on the US east coast.

Equipment:

Shippers should still expect a delay of around three days waiting to collect containers once discharged.

Ports

CMA CGM has announced a port congestion surcharge of US$250 per TEU for all types of cargo from Latin America to the Port of Oakland in the United States.

The port of Long Beach has signed a four-year partnership agreement with the Utah Inland Port Authority (UIPA) in an effort to ease congestion in the long term.

Asia → Europe (Far East Westbound)

Rates

SCFI (Spot rate Index) to North Europe reached next record of 6,479USD/TEU for Week 25/2021

Following GRIs announced last week, rates now sit between $14,000-15,000 for the majority of carriers and $19,500 for MSC in the first half of July.

Capacity

Capacity expected to remain tight going into peak season as sufficient demand remains to outperform max capacity.

CMA, COSCO and MSC have canceled space previously released.

Chinese ports are still dealing with a backlog from Yantian disruption

Yantian reports a waiting time of 7 days to berth

Shakou reports a waiting time of 4 days to berth

Equipment

There is currently a severe shortage of 40ft high cubes, but still availability for standard 40ft containers.

There is also available stock of 20ft containers.

Ports

Rotterdam remains congested, with both Ocean Alliance and THE Alliance omitting calls, with the former also missing Flexistowe.

A shortage of truck drivers in the UK is causing delays in getting containers out of ports.

Carriers

POL

20GP

40GP

40HQ

HPL

NINGBO

Shortage

Shortage

Shortage

SHANGHAI

Shortage

Normal

Shortage

YANTIAN

Normal

Normal

Shortage

SHEKOU

Normal

Shortage

Shortage

MSK

QINGDAO

Shortage

Shortage

Shortage

SHANGHAI

Shortage

Shortage

Shortage

NINGBO

Shortage

Shortage

Shortage

Nanjing

Shortage

Normal

Shortage

Xiamen

Shortage

Normal

Shortage

YANTIAN

Normal

Normal

Shortage

SHEKOU

Normal

Shortage

Shortage

NANSHA

Normal

Normal

Shortage

HONGKONG

Normal

Normal

Shortage

SHANTOU

Normal

Normal

Shortage

ONE

YANTIAN

Normal

Normal

Normal

SHEKOU

Normal

Normal

Shortage

XINGANG

Normal

Shortage

Shortage

QINGDAO

Normal

Normal

Shortage

SHANGHAI

Normal

Normal

Normal

NINGBO

Shortage

Shortage

Shortage

ZIM

XIANGANG

Normal

Shortage

Shortage

NINGBO

Normal

Shortage

Shortage

SHANGHAI

Normal

Shortage

Shortage

YANTIAN

Normal

Shortage

Shortage

SHEKOU

Normal

Shortage

Shortage

HMM

SHANGHAI

Normal

Normal

Shortage

NINGBO

Normal

Shortage

Shortage

YANTIAN

Normal

Normal

Shortage

SHEKOU

Normal

Normal

Shortage

MSC

SHANGHAI

Normal

Shortage

Shortage

NINGBO

Shortage

Normal

Shortage

YANTIAN

Normal

Shortage

Shortage

SHEKOU

Shortage

Normal

Shortage

EMC

YANTIAN

Normal

Normal

Shortage

SHEKOU

Shortage

Normal

Shortage

NINGBO

Shortage

Normal

Shortage

SHANGHAI

Normal

Shortage

Shortage

QINGDAO

Normal

Shortage

Shortage

OOCL

YANTIAN

Normal

Normal

Normal

SHANGHAI

Normal

Normal

Normal

NINGBO

Normal

Normal

Normal

CMA

QINGDAO

Shortage

Shortage

Shortage

SHANGHAI

Shortage

Shortage

Shortage

NINGBO

Shortage

Shortage

Shortage

YANTIAN

Shortage

Shortage

Shortage

SHEKOU

Shortage

Shortage

Shortage

cosco

YANTIAN

Normal

Normal

Normal

SHEKOU

Normal

Normal

Normal

SHANGHAI

Normal

Normal

Shortage

NINGBO

Normal

Normal

Shortage

QINGDAO

Normal

Normal

Shortage

DALIAN

Normal

Normal

Normal

XINGANG

Normal

Normal

Normal

YML

YANTIAN

Normal

Normal

Shortage

SHEKOU

Normal

Normal

Shortage

Europe → USA (Transatlantic Westbound)

Rates

CMA has announced a new PSS from Europe to North America, effective from August 1st:

East Coast: $1,000/ 20′, $1,250/ 40′

West Coast: $1,000 /20′, $1,500/ 40′

Strong volume performance and cargo backlog are likely to drive rates further up during Q3

Capacity:

ONE and Yang Ming are reported to not have space until mid-August, though MSC have some pockets of space.

A streak of blank sailings due to vessel maintenance will be implemented by THE Alliance and Ocean Alliance in week 29 and 31 on the USWC service.

Ports:

Hapag-Lloyd have announced a Congestion Surcharge of USD 350 per container for all intermodal moves in the US effective upon carrier receipt of cargo on or after August 1, 2021 until further notice.

Air

Asia

US market

Space and rate situation out of China is critical this week as worsening congestion and capacity issues add to backlogs of ocean freight cargo and increase the volumes of ocean to air freight conversions.

Only highest paying cargo is guaranteed to make it on to a flight

Some converted passenger flights are being changed to domestic flights to accommodate summer holiday travel

Spot rates available for heavy/dense cargo as well as volume cargo.

For all airports – rates and space must be checked on a case by case basis.

EU market (base airport like FRA/AMS/LUX, etc)

Space and rate situation out of China is critical this week as worsening congestion and capacity issues add to backlogs of ocean freight cargo and increase the volumes of ocean to air freight conversions.

Only highest paying cargo is guaranteed to make it on to a flight

Some converted passenger flights are being changed to domestic flights to accommodate summer holiday travel

Rates and space must be checked on a case by case basis.

Spot rates available for heavy/dense cargo as well as volume cargo.

UK market

Space and rate situation out of China is critical this week as worsening congestion and capacity issues add to backlogs of ocean freight cargo and increase the volumes of ocean to air freight conversions.

Only highest paying cargo is guaranteed to make it on to a flight

Some converted passenger flights are being changed to domestic flights to accommodate summer holiday travel

There are direct flights with CA/BA, AIR-AIR by SQ and normal air-truck service. Space using deferred carriers is fully booked.

Rates and space must be checked on a case by case basis.

Spot rates available for heavy/dense cargo as well as volume cargo.

Americas

Rates have increased 20-30% in the last week into UK, Europe and Asia

Space remains constricted due to reduced capacity.

There are still backlogs at the handling sheds at main airports, resulting in long queues when collecting/delivering cargo. This will only get worse when the new screening regulations come into play on 1st July.

US hauliers are currently over capacity and over booked causing more delays.

Europe

Rates into North America have increased this week, while rates into Asia remain stable.

Capacity to most regions remains severely restricted

Road

Availability

Availability generally reliable across all routes and regions.

Rates

Rates are fluctuating in and out of Italy, but remain stable across consolidated, groupage and dedicated trailers on other routes.

Customs

Border situations have improved considerably with clearances running smoothly.

The route ahead

The information that is available in the Weekly Market Update comes from a variety of online sources, partners and our own teams. Click below to learn more about how Zencargo can help make your supply chain your competitive advantage.